How long can markets remain resilient?

Views & insightsWe examine how markets have remained resilient amidst the geopolitical uncertainty stemming from the U.S.-Iran conflict.

Key highlights

- Markets react to U.S.-Iran negotiations: Reports of an agreement for Iran to hand over its stockpile of highly enriched uranium had a positive effect on global equity markets.

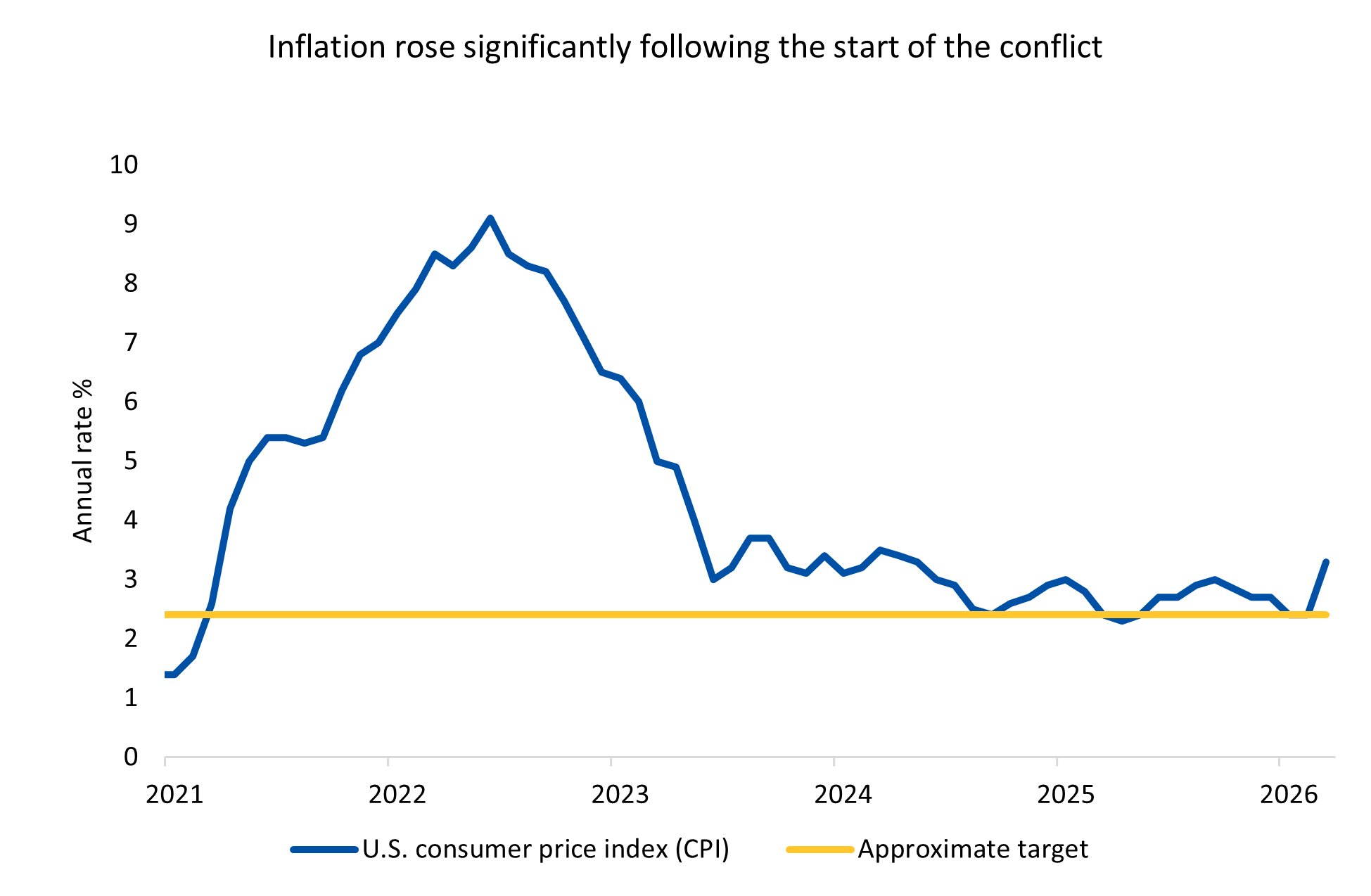

- U.S. inflation jumps: Consumer price index (CPI) data for March showed headline inflation jumped to 3.3% year-on-year. This was primarily driven by a 20% month-on-month spike in energy commodities.

- UK growth remains resilient: UK monthly GDP data for February came in surprisingly strong at 0.5% month-on-month, reflecting an improvement in household confidence.

Blockades to breakthroughs

The Middle East conflict remained the focus last week.

Following the breakdown of U.S.-Iran negotiations, last week the U.S. imposed a naval blockade on Iranian ports and coastal areas. This represented a shift in strategy from the previously threatened strikes on domestic Iranian energy infrastructure. This pivot was reportedly driven by U.S. Central Command’s concerns over the depletion of munitions stocks required to sustain a prolonged bombing campaign.

The blockade’s practical enforcement was tested early in the week, with markets closely watching the passage of the Rich Starry – a Chinese-owned, Malawian-flagged vessel previously blacklisted for sanctions violations – through the Strait of Hormuz. The ship ultimately turned back, suggesting the blockade is, for the time being, holding. Tanker traffic through the Strait has effectively been curtailed.

The geopolitical calculus remains complex. Helima Croft of RBC Capital Markets cautioned against assuming China would pressure Iran toward a deal. She noted that Beijing has amassed significant energy stockpiles and may view the redeployment of U.S. military assets away from Asia – and the running down of American missile inventories – as a net strategic benefit. On the other hand, the blockade imposes real economic costs to the Chinese energy supply, which doesn’t improve the already strained bilateral relationship between Washington and Beijing.

By mid-week, however, sentiment shifted materially. President Donald Trump indicated that Iran had reached out to resume peace negotiations, with reports suggesting face-to-face talks would occur before the current ceasefire expires next week.

Over the last week, negotiations have continued on a number of official and unofficial fronts. Specific parameters related to Iran’s nuclear programme remain contentious, but as both parties are evidently able to restrict access to the Strait of Hormuz, it becomes harder for either one to use that as leverage. Over the weekend, the Strait appeared to have been reopened by Iran, but it was closed again as the U.S. failed to lift the blockade. These developments serve as a reason for optimism regarding a mutually beneficial agreement potentially being reached this week.

The market reaction to these developments was notably restrained throughout the week. Equity volatility indices fell back to levels consistent with those prevailing before the conflict’s onset, and an increasing number of global indices moved into positive territory relative to the start of hostilities. Brent crude, while still elevated at approximately $94 per barrel, eased from its highs as the prospect of a diplomatic resolution introduced fresh supply expectations.

There’s no question that markets appear complacent considering the significant economic risks that remain. It seems likely that the market reaction has more to do with the continued flow of new funds into markets, driven mainly by employment compensation, than with an appraisal of the earning potential of most companies.

The weekly employment data released, which runs up to 11 April, showed that there has been no discernible increase in job losses since the conflict began. While employment remains reasonably strong, pension contributions will continue to push stocks higher.

Companies that had stopped buybacks ahead of their earnings releases will be able to return to the market once they’ve reported, which will likely provide additional support for the markets.

The earnings season properly began last week and will step up this week.

U.S. inflation: Accelerating from an elevated base

Source: Bloomberg

The main concern for investors has been the risk of inflation. It detracts from growth and increases potential interest rates.

In the U.S., CPI data for March has shown an acceleration in headline inflation, jumping to 3.3% year-on-year. Unsurprisingly, the primary driver was a spike of over 20% month-on-month in the energy commodity category. This represents the largest increase in the history of the data series, which extends back to the late 1950s. There were early signs of energy cost pass-through, most visibly in airfares, but critically, there has been no evidence yet of broad-based contagion.

The conflict isn’t the only factor affecting inflation. AI, for example, is both disinflationary and inflationary. While there’s an expectation that AI will suppress ‘white collar’ wages and, thus, services inflation, AI-related demand has driven computer memory prices up over 2,000% in the past year and therefore maintained upward pressure on tech hardware prices.

What will the implications of this be for Federal Reserve (the Fed) policy? Markets are now pricing in the possibility of a single cut in the Fed funds rate through year-end. With inflation accelerating from an already elevated level, and having missed its target for an extended period, the Fed will require clear, sustained evidence of economic weakening before cutting rates.

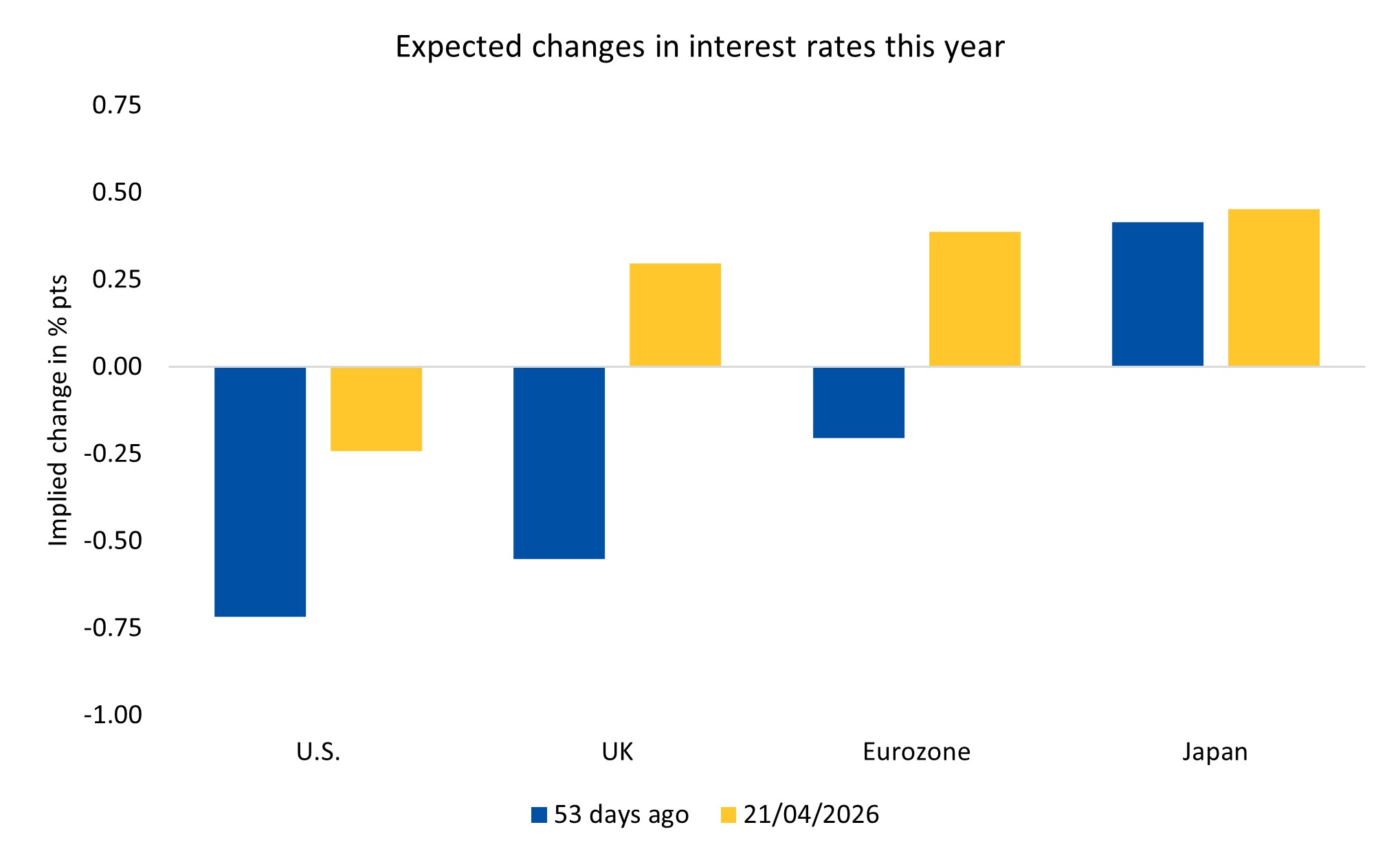

Source: Bloomberg

Two factors will be decisive.

First, the consumer: spending growth has held up at 2.5% year-on-year, but income growth has weakened to just 1%, pushing the savings rate down to a historically low 4%. Bank of America deposit data reveals a stark K-shaped divergence – higher earners are seeing wage growth near 6%, while lower earners are at approximately 1%. Given that lower income households have a higher marginal propensity to spend, this divergence represents a meaningful risk to the consumption outlook.

Second, inflation expectations: market-based measures, such as five-year forward expectations, remain well-anchored, and survey-based measures show only a modest uptick – nothing alarming thus far.

UK: Growth remains resilient, but headwinds are gathering

UK monthly GDP data for February came in surprisingly strong at 0.5% month-on-month, reflecting an improvement in household confidence following the widely feared Autumn Budget.

However, this pace isn’t considered sustainable, and the data pre-dates the onset of the Middle East conflict. Purchasing Managers Indices (PMI) readings have already softened, and elevated energy costs are expected to take the sting out of the year’s strong start.

The government announced a £600 million package of deferred costs for manufacturing businesses to help manage higher input cost inflation – a modest but directionally positive measure.

UK wage growth remains stubbornly above levels consistent with the Bank of England’s 2% target, effectively ruling out near-term rate cuts. Markets now expect one to two rate hikes by year-end, and gilt yields have risen accordingly. Sterling has maintained a firm footing near $1.35, supported by the expectation of sustained higher rates.

Political risk has also entered the frame. The revelation that former U.S. ambassador Peter Mandelson failed the vetting process has placed additional pressure on Prime Minister Sir Keir Starmer. Prediction markets are now seeing the probability of Sir Keir’s departure by year-end jump from approximately 40% to 55–60%. This uncertainty contributed to gilts underperforming other European sovereign bonds.

Coming up

- U.S.-Iran cease fire: Will the ceasefire hold and will the Strait of Hormuz be reopened? This will be the main concern for markets.

- UK house prices: Rightmove data will show how house prices are holding up now that mortgages have become more expensive.

- UK jobs data: The U.S. labour market is holding up well, but it remains to be seen how European labour markets will fare with higher energy prices.

The value of investments, and any income from them, can fall and you may get back less than you invested. Neither simulated nor actual past performance are reliable indicators of future performance. Investment values may increase or decrease as a result of currency fluctuations. Information is provided only as an example and is not a recommendation to pursue a particular strategy. Information contained in this document is believed to be reliable and accurate, but without further investigation cannot be warranted as to accuracy or completeness. Forecasts are not a reliable indicator of future performance. We or a connected person may have positions in or options on the securities mentioned herein or may buy, sell or offer to make a purchase or sale of such securities from time to time. For further information, please refer to our conflicts policy which is available on request or can be accessed via our website at www.brewin.co.uk.